The Subsea Compounder

Mispriced dominance in the subsea world

Every now and then you come across a business that makes you stop and check the valuation twice.

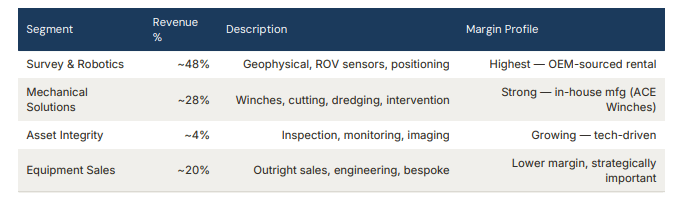

Founded in Aberdeen in 1985, the company started life renting specialist subsea survey equipment to oil and gas operators in the North Sea. Forty years later, it has quietly grown into the dominant player in global subsea equipment rental — operating a fleet of over 30,000 assets across sixteen facilities in key offshore energy hubs worldwide. Its three service lines — Survey & Robotics, Mechanical Solutions, and Asset Integrity — give clients a one-stop shop for everything from seabed surveying to decommissioning, with over 85% of the equipment fungible across oil & gas and offshore wind. No other competitor can offer that kind of integrated package.

And yet the stock trades like a structurally declining business.

We think the market has this one badly wrong. Below, we lay out why Ashtead Technology is one of the most compelling risk/reward opportunities in UK small-caps today.

If you've been enjoying the research, I'd greatly appreciate it if you hit the share button below. My goal is to grow this publication into a community of like-minded investors where we share ideas transparently, challenge each other's thinking, and debate the things that actually matter. Every share helps make that happen.

Investment Thesis

The market is pricing Ashtead Technology like a cyclical oil services company nearing peak earnings. It is not. This is a capital-light rental compounder with a dominant market position, 25–30% of the global subsea equipment rental market, EBIT margins above 25%, returns on invested capital above 22%, and a 20-year track record of profitable growth through the cycle — including double-digit EBIT margins in the 2015–16 oil price collapse.

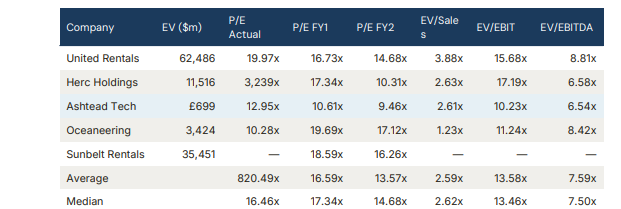

Since its M&A strategy was launched in 2017, the company has compounded revenues at 45% and EBITA at 63%. Since IPO in 2021, adjusted EPS has compounded at 37% CAGR. The stock has re-rated from its trough (up ~30% from February lows) but at 10.6x FY1 P/E and 6.5x EV/EBITDA, it still trades well below both its own 5-year median (12.1x EV/EBITDA) and every peer in the comps group.

The disconnect is the opportunity. Ashtead Technology is building the Ashtead Group (the equipment rental giant) of the subsea world — rolling up a fragmented market, improving utilisation on acquired assets, and expanding into offshore renewables. The market either does not understand the durability of the model or is applying an unwarranted cyclical discount to a company with demonstrated through-cycle resilience. At current prices, the risk/reward is compelling.

How Ashtead Makes Money

Ashtead is a global subsea equipment rental and solutions provider, headquartered in Aberdeen, Scotland, serving the offshore energy sector. Founded in 1985, the company provides mission-critical equipment used in the inspection, construction, maintenance, and decommissioning of subsea infrastructure — primarily oil and gas assets and, increasingly, offshore wind installations.

The business model is elegant. Ashtead owns a fleet of over 23,000 specialised subsea assets — survey instruments, ROV sensors, mechanical tools, winches, and dredging equipment — and rents them to offshore energy contractors on a project basis. Approximately 80% of revenue comes from equipment rentals, with the remaining ~20% from equipment sales and engineering services. Utilisation rates consistently exceed 75%, underpinning revenue stability and strong returns.

The client base comprises blue-chip offshore contractors — Subsea7, Saipem, TechnipFMC — and energy majors. Ashtead operates from 12 strategic hubs across the UK, Norway, US, Brazil, UAE, and Singapore. In FY2025, 33% of revenue was generated outside Europe.

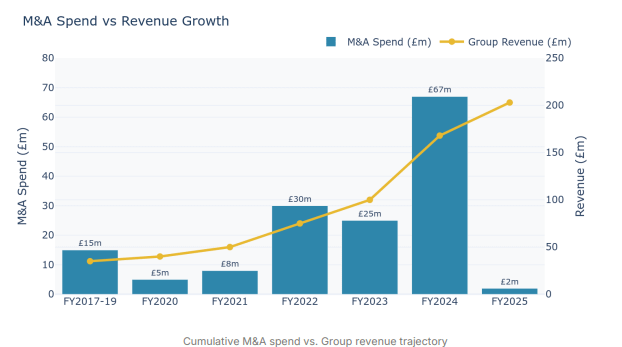

CEO Allan Pirie has overseen the transformation from a regional rental house into a global subsea services leader. The management team has a strong M&A track record — nine acquisitions in seven years, all integrated successfully and at attractive multiples averaging 4.6x EBITDA. Capital allocation discipline is a hallmark: growth is funded through operating cash flow and the revolving credit facility, with zero equity dilution since IPO.

The Sector: Competitive Landscape & Strategic Positioning

The global subsea equipment rental market was valued at approximately USD 3.6 billion in 2025, with a projected CAGR of 5.4% to reach USD 5.2 billion by 2032. Growth is driven by increasing deepwater drilling activity, offshore wind development, ageing subsea infrastructure requiring inspection and maintenance, and a structural shift toward rental over ownership among offshore contractors.

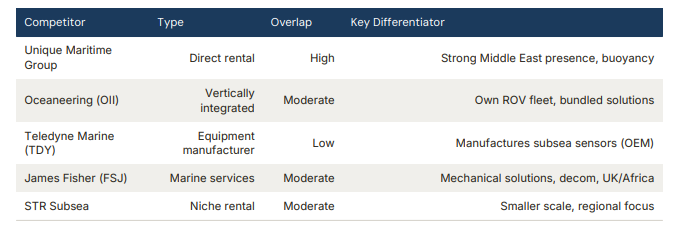

The market is increasingly an oligopoly. Ashtead Technology controls an estimated 25–30% of the global subsea equipment rental market. Following its acquisition of Seatronics from Acteon Group, the top three players now account for a substantial majority of the market.1 Unique Maritime Group and STR hold the next ~30% combined.

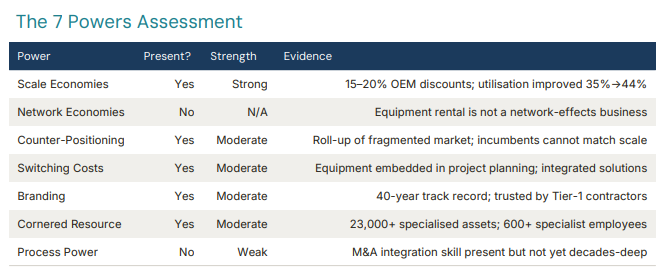

Scale Economies are the most important power. Ashtead's 25–30% market share generates meaningful unit cost advantages: 15–20% purchasing discounts from OEM suppliers, higher fleet utilisation (above 75%), and the ability to improve utilisation on acquired businesses over time. Cost utilisation improved from 35% in 2019 (post-acquisition dip) to 44% currently.

Counter-Positioning is underappreciated. Ashtead is executing a roll-up of a fragmented market. Its acquisition strategy — buying at 5–7x EBITDA, integrating, and improving utilisation — creates a flywheel that smaller competitors cannot replicate. The Seatronics/J2 Subsea acquisition removed a direct competitor from the market entirely.

Financial Summary

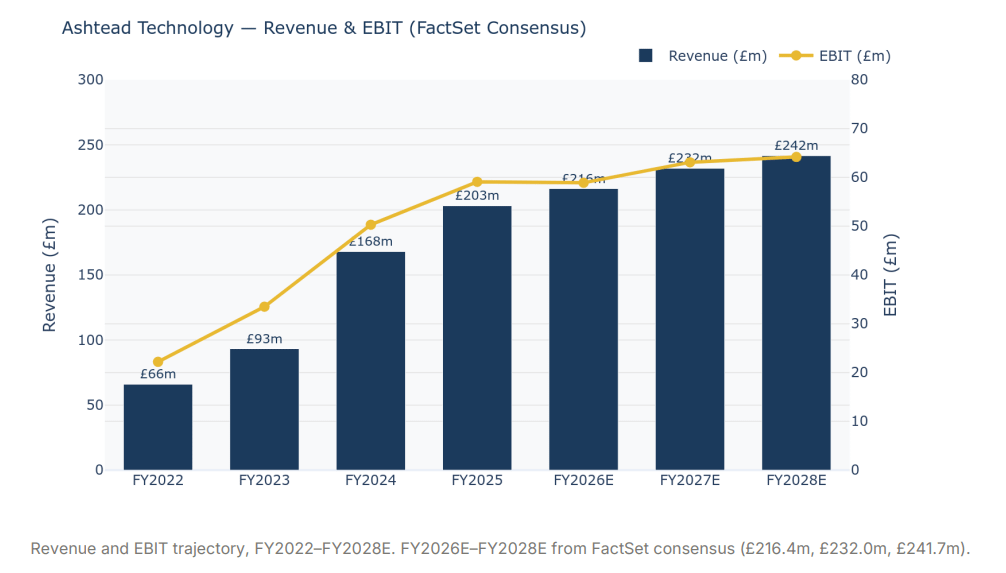

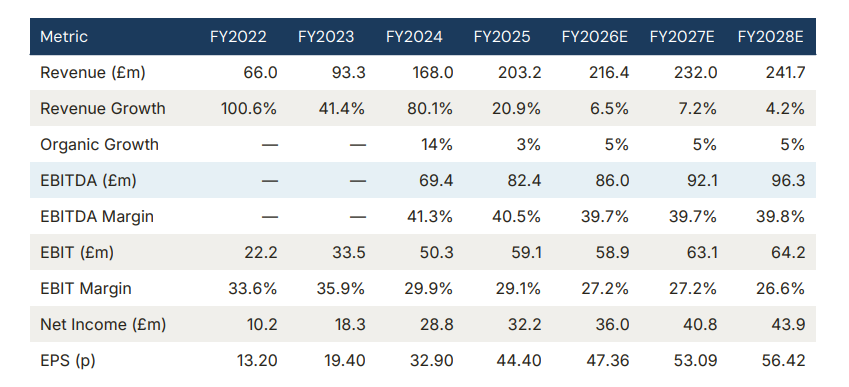

FY2025 revenue of £203.2m represented 21% growth YoY, decomposing as:

Organic growth: +3% — solid against a backdrop of Middle East geopolitical disruption

Inorganic growth: +19% — full-year contribution from Seatronics and J2 Subsea

FX headwind: -1% — sterling strength vs USD

FactSet consensus implies FY2026E revenue of £216.4m, a 6.5% increase — a normalisation year as the inorganic tailwind from Seatronics and J2 Subsea anniversaries and the group reverts to its organic growth rate of ~5%. FY2027E (£232.0m, +7.2%) and FY2028E (£241.7m, +4.2%) show stable, modest growth as the business matures. Rystad Energy data and customers' growing backlogs support the medium-term organic growth outlook.

Sector diversification is critical. Offshore renewables now represent approximately 30% of group revenue, up materially from a historically oil and gas-dominated mix. Management targets 40% from green energy by end-2026, driven by offshore wind construction, structural monitoring, and subsea cable protection services.

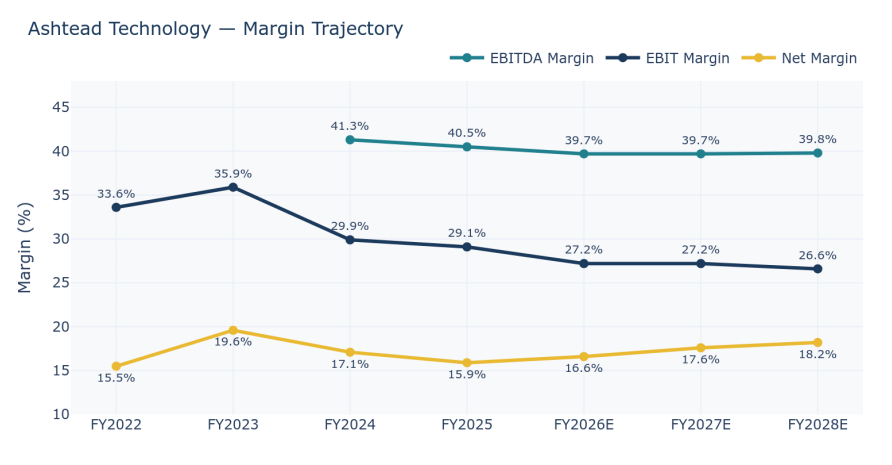

FactSet consensus shows Ashtead Technology's FY2025 EBITDA margin at 40.5% and FY2026E EBITDA margin at 39.7% — essentially flat, indicating margin stability despite the revenue growth mix shift.3 EBIT margin (FY2025: 29.1%, FY2026E: 27.2%) reflects slightly higher D&A as the acquired asset base grows, but EBITDA margins remain anchored near 40%.

Consensus shows Ashtead Technology's actual EBITDA margin at 39.9% and NTM EBITDA margin at 39.7% — essentially flat, indicating margin stability despite the revenue growth mix shift. EBIT margin (actual 25.5%, NTM 27.2%) shows improvement, suggesting operating leverage is emerging as integration synergies flow through.

Ashtead Technology's EBIT margin of 29.1% is the highest in the peer group, comfortably above United Rentals (24.8%), and more than double Oceaneering (10.9%). The company's net margin of 15.9% is also best-in-class, underscoring the capital efficiency of the rental model.

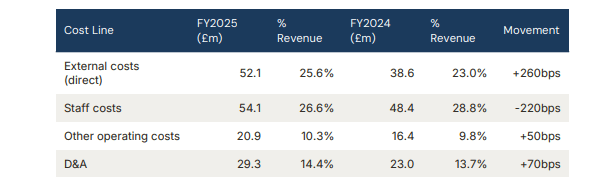

Staff cost leverage (from 28.8% to 26.6%) is the standout — the Seatronics integration brought 110 people but revenue scaled faster, demonstrating operating leverage on the fixed cost base.

Net debt reduced to £108.9m from £128.4m, bringing proforma leverage to 1.3x — providing significant strategic optionality for the next acquisition.7 Capital allocation priorities are well-ordered: (1) organic reinvestment, (2) bolt-on M&A at 5–7x EBITDA, (3) progressive dividend, (4) balance sheet strength.

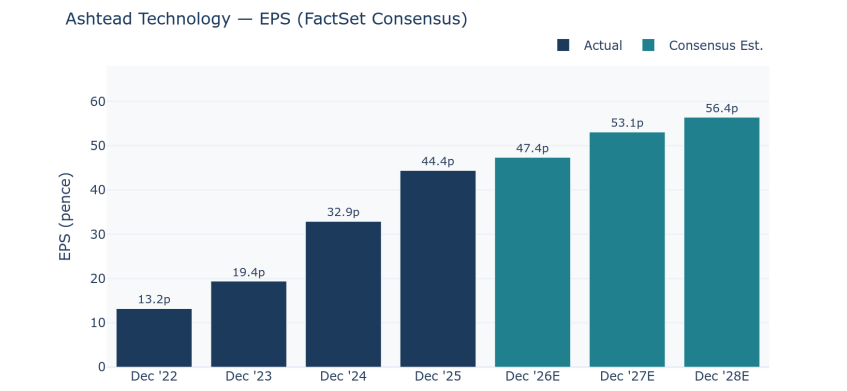

EPS Estimates & Consensus

FactSet consensus for Dec ’26E EPS stands at 47.36p (9 analysts, range 43.30–51.70p) as of 17 April 2026.3 This compares to Dec ’25 actual EPS of 44.40p, implying ~6.7% EPS growth year-on-year. Estimates for Dec ’27E through Dec ’28E show a resumption of growth, reaching 56.42p by FY2028E.

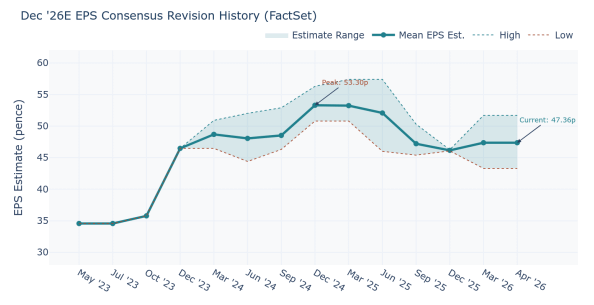

Dec ’26E consensus has fallen ~11% from its peak of 53.30p (December 2024) to 47.36p today.3 The downward revision cycle coincided with Middle East project delays and softer-than-expected organic growth in H2 FY2025. However, estimates have stabilised since January 2026 (47.17p → 47.36p over three months), suggesting the revision cycle may be bottoming.

Valuation

The valuation anomaly persists even after the recent share price rally. Ashtead Technology trades at the lowest P/E and EV/EBITDA multiple in the peer group despite having the highest EBIT margins and strongest competitive positioning.

At 10.6x FY1 P/E, Ashtead trades at a 37% discount to the peer median (16.46x). On EV/EBITDA, the 6.54x multiple sits 13% below the peer median (7.50x) and well below United Rentals at 8.81x. The EV/EBIT of 10.23x vs. the peer median of 13.46x represents a 24% discount despite Ashtead having the highest EBIT margin in the group (25.5%).

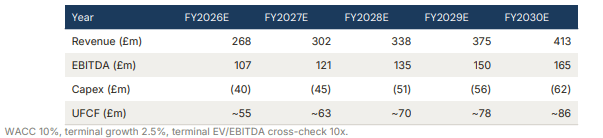

DCF implies an equity value of £750–850m, or 930–1,050p per share — roughly 85–105% upside from the current price.

Multiple re-rating target: Applying the peer median 7.5x EV/EBITDA to FY2026E EBITDA of £106.9m yields EV of ~£802m. Deducting ~£90m net debt and dividing by ~81m shares implies ~879p (+73%). At the company's own 5-year median of 12.1x, the implied price exceeds 1,300p.

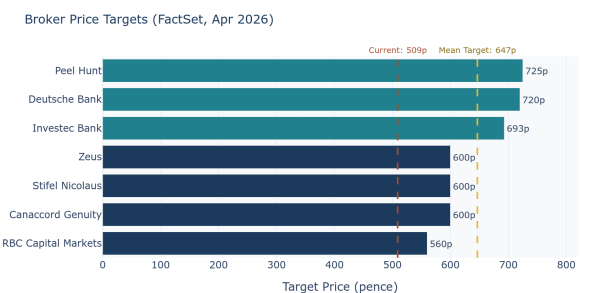

All 9 covering analysts rate Ashtead Technology a Buy. The mean price target of 646.56p implies 27.1% upside from the current 509p. The range spans 560p (RBC Capital Markets) to 725p (Peel Hunt).

What the Street Is Missing

Through-cycle resilience is underappreciated. Double-digit EBIT margins even in 2015–16 oil collapse. This is not a typical cyclical business.

The renewables pivot is real. 30% of revenue from offshore renewables de-risks the oil dependency narrative.

EPS revisions are stabilising. After an 11% decline from Dec ’24 peak, consensus has flatlined for three months (47.17p → 47.36p). If organic growth re-accelerates, upward revisions would drive a re-rating.

The AIM-to-Main Market transition should broaden the investor base and drive passive buying flows as FTSE index inclusion becomes possible.

M&A optionality is mispriced. At 1.3x leverage, the balance sheet can support a transformational deal that consensus does not model.

Key Risks

Oil price cyclicality. A sustained downturn could slow offshore capex. Mitigated by renewables diversification (~30% of revenue) and maintenance/decommissioning demand.

Negative EPS revisions could continue. Consensus has already fallen 11% from peak. If organic growth disappoints further, the revision cycle could deepen.

Middle East geopolitical volatility. Management flagged project timing uncertainty.

M&A integration and execution risk. Strategy depends on continued successful acquisitions. Mitigant: 9 successful integrations with no equity dilution.

Key person risk. CEO Allan Pirie has been central to the transformation.

Technology disruption. AI-driven autonomous inspection could disrupt the rental model if Ashtead fails to invest in digital capabilities.

Catalysts & Timeline

FY2026 interim results (H1 2026) — Opportunity to demonstrate organic growth recovery and margin stability

Further M&A announcements — Active pipeline; 1.3x leverage supports meaningful deals

Main Market / FTSE index inclusion — Would drive passive buying flows • Offshore wind contract wins — Tier-1 EPCI awards would validate renewables pivot

EPS revision inflection — Stabilisation is here; first positive revision would signal bottoming

Oil price recovery / stability — Accelerates near-term organic growth

The Bottom Line

Ashtead Technology is a market-leading compounder trading at a 37% P/E discount to its peer group median. The business has 25–30% share of a growing oligopoly, EBIT margins above 25%, a proven M&A playbook delivering 20%+ ROIC, and a diversification strategy into offshore renewables gaining real traction. All 9 analysts covering the stock rate it Buy with a mean target of 647p. EPS revisions have stabilised after an 11% decline. At 10.6x FY1 earnings, the market is offering a rare chance to own a high-quality compounder at a price that assumes the growth story is over. It is not.

Thanks for reading. Subscribe for more deep-dive special situations, underfollowed small caps, and mispriced equities.

- Uncovered Alpha

Disclosure: This note reflects our opinion as of the publication date and is provided for informational purposes only. It is not personalized investment advice or a recommendation to buy or sell any security. We may hold positions in securities discussed. Always do your own work and consult a qualified adviser where appropriate.

Your 2026 estimates are wrong - https://www.ashtead-technology.com/investors/analyst-consensus/