Expendable Everything: Making Sense of the Military Drone Market

What This Is — and Why We Wrote It

This piece steps outside the usual lane. I usually cover consumer discretionary and industrials—not defence, not aerospace, and certainly not small-cap hardware companies burning $100m of cash per year. But occasionally a structural shift in another sector becomes large enough, and its financial implications compelling enough, that it warrants the detour.

The military drone market is that moment.

The goal here is straightforward: to give readers a working framework for the drone sector — how the market is structured, what the key technology segments actually mean, who the major public and private players are, and where value creation is most likely to occur. Against that backdrop, Red Cat Holdings (NASDAQ:RCAT) has emerged as one of the more interesting smaller names in the publicly listed universe —a company that has won a meaningful US Army programme-of-record contract and is scaling rapidly into what looks like a structurally growing market.

This is not a formal initiation of coverage. Think of it as the first instalment of a deeper look. Red Cat merits more rigorous scrutiny than a single note can provide, and this piece is designed to build the foundation for that work. Future analysis will dig further into the unit economics, the competitive dynamics around the Army SRR programme, and what a realistic path to profitability actually looks like.

Why the Drone Market Is Interesting Right Now

The case for paying attention to the military drone sector rests on five overlapping observations. None of them individually is sufficient. Together, they build a thesis.

Iran changed the conversation permanently

Ukraine demonstrated that cheap, mass-produced drones could reshape tactical warfare. Iran has since demonstrated that the same logic applies at the strategic level. Since the onset of Operation Epic Fury, Iran has launched more than 3,600 one-way attack drones against US forces and allied targets. The saturation has exposed a fundamental vulnerability: advanced Western air defence architectures — built around expensive interceptor missiles — are economically unsustainable against mass drone attacks.

The arithmetic is brutal. A Patriot PAC-3 interceptor costs north of $3m per shot. A Shahed-136 drone costs roughly $30,000. At a ratio of 100:1 in unit cost terms, an adversary deploying thousands of drones can exhaust a defender’s magazine before attriting the attacking force. This is not a future risk. It is a live operational problem that the DoD, NATO allies, and every serious defence ministry in the world is currently working to solve.

The US response has been to accelerate its own low-cost expendable arsenal. The LUCAS — a reverse-engineered Shahed derivative — was embedded at US Central Command in December 2025 after being pushed through the acquisition pipeline in just 18 months and deployed operationally in the opening wave of Epic Fury. That speed of procurement is almost without historical precedent in US defence acquisition. It signals how urgent the need has become.

Defence budget allocation is structurally shifting toward unmanned systems

The US DoD’s FY26 budget request includes $14bn for unmanned and autonomous platforms, of which $9.4bn is for aerial drones including collaborative combat aircraft (CCAs). The US Army’s small drone budget for FY26 recorded an eightfold increase relative to FY24 and FY25, reaching $804m — reflecting the service’s recognition that every soldier at the squad and platoon level needs organic ISR and strike capability.

Under the “Unleashing American Drone Dominance” executive order of June 2025, a new procurement programme was launched in November calling for 340,000 small strike drones by 2028 — phased across four tranches, starting at $5,000 per unit in early 2026 and compressing to $2,300 by late 2027 as volumes scale. Total programme value: $1bn. This is the kind of demand signal that turns small-cap drone companies into mid-cap ones.

The commercial and strategic drone market is early innings, not mature

The global military UAS market is currently sized at $13–16bn, growing to $21–27bn by 2030 at a consensus ~9% CAGR drawn from eight independent research firms. These estimates are almost certainly conservative — they were built before the Iran conflict made drone procurement an acute, non-negotiable strategic priority. Defence research firms that sized the 2032 market at $16.4bn in 2022–23 had already revised that estimate to $27.5bn in their 2024–25 editions, a 67% upward revision in two years. Another material upward revision is likely when post-Epic Fury procurement plans are fully incorporated.

Viewed against global defence spending — which reached $2.7tn in 2024 according to SIPRI — drones currently represent roughly 2–3% of total equipment budgets. That share is going to grow. The question is how fast, and who captures it.

Western supply chains are being rebuilt from scratch

China’s DJI is estimated to have generated approximately $11bn in revenue in 2024. It dominates commercial drone hardware globally. It is effectively locked out of US and allied government procurement by NDAA restrictions barring Chinese-component drone systems. That creates a large, structured market opportunity for American and allied manufacturers to fill — not by competing with DJI on cost, but by offering NDAA-compliant, Blue UAS-certified systems that government buyers have no alternative but to procure domestically.

This is not a tariff story or a trade war story. It is a strategic autonomy story. Western governments have decided they will not depend on Chinese drone hardware for national security purposes. That structural decision creates durable demand for domestic producers regardless of the broader macro or geopolitical environment.

The listed universe is still thin — information advantages exist

The publicly traded pure-play drone universe in the US remains small: AeroVironment, Kratos, Ondas, Unusual Machines, and Red Cat are the primary names. Coverage is sparse, institutional ownership is limited, and analytical frameworks are still being built. In sectors like this — where the fundamentals are moving fast and the market is still developing its understanding — research quality is a genuine differentiator. That is part of what motivates this piece.

Understanding the Market: A Taxonomy That Actually Helps

Before turning to individual companies, it is worth grounding the framework. “Drone” means very different things across different segments, and the investment characteristics vary sharply by category.

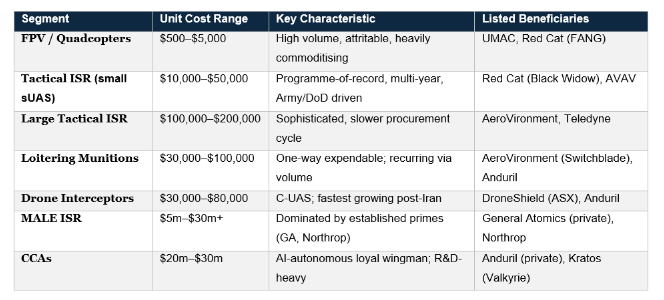

How to Think About the Market Segments

The official military taxonomy — NATO Class I, II, III; US DoD Groups 1 through 5 — is useful for understanding vehicle size and operating altitude, but it tells you little about what matters most for investors: what the drone does, how much it costs, and what the demand driver is.

A more useful framework organises by mission type:

The strategic insight from this framework: the highest-quality investment opportunities for smaller listed companies sit in the tactical ISR and loitering munitions segments. These are large enough in volume to drive meaningful revenue, short enough in procurement cycle to have near-term visibility, and technically specialised enough that NDAA compliance provides genuine competitive protection.

The FPV/quadcopter segment is a trap for investors who conflate volume with value. Unit economics are commodity-like, Chinese producers have an overwhelming cost advantage in the non-government market, and the segment is heavily dependent on active conflict for consumption velocity. Once the Ukraine conflict ends, mature Ukrainian FPV producers will likely pivot to European export, further compressing prices. FANG and similar US FPV products survive in the listed domain only because of NDAA compliance — without it, there is no business.

At the other extreme, MALE ISR and CCA programmes remain the domain of established Tier 1 primes. The capital requirements, certification timelines, and customer relationship depth needed to compete for a $10bn MALE programme are beyond the reach of any publicly listed small-cap drone company.

The Doctrine Behind the Budget

One of the clearest signals from both the Ukraine conflict and the Iran campaign is that sophistication is not the most important feature of a battlefield drone. Industry data suggests a drone survives an average of fewer than five flights in a contested environment. Drones designed before 2022 — built to be sophisticated, expensive, and recoverable — have proved too costly to expose and too slow to produce in the required volumes.

The new doctrine can be summarised simply: mass, cheap, autonomous, NDAA-compliant, attritable. A swarm of 200 $3,000 drones will consistently defeat a pair of $200,000 ones in a contested airspace environment. The DoD’s 340,000-drone programme is the institutional expression of that conclusion.

AI is the technology layer that makes this doctrine operationally viable. Without AI-aided autonomous navigation, target recognition, and swarm coordination, cheap drones require one human operator per vehicle. The AI layer removes that constraint. It is also the technology layer most insulated from commodity competition — model weights and autonomy software cannot be easily replicated by a low-cost hardware producer.

The Public Universe: Who Matters

AeroVironment (NASDAQ: AVAV) — The Incumbent

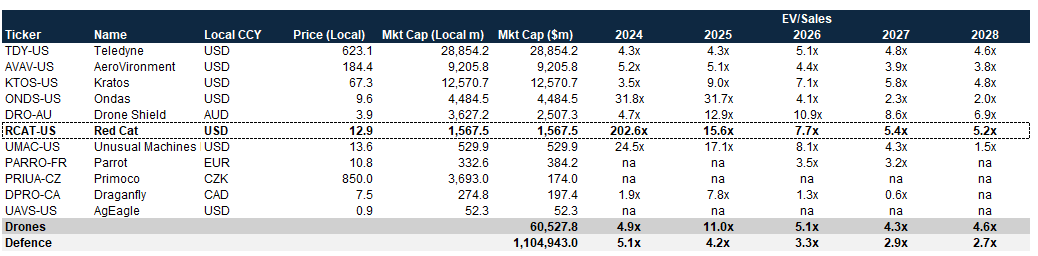

AeroVironment is the most established pure-play drone company in the listed US universe at a $9.2bn market cap. It supplies the Puma, Raven, and Switchblade systems across multiple US and allied military programmes, and was selected for the Replicator Initiative with its Switchblade 600 loitering munition. It is the quality benchmark — a company with demonstrated programme-of-record delivery history, strong gross margins, and a track record of navigating DoD procurement cycles. It also carries a valuation that reflects that quality: 4.4x FY26E EV/Sales versus a drone peer group average of 7–8x. For long-term investors in the sector wanting a lower-risk, lower-volatility entry point, AVAV is the natural first stop.

Kratos Defence (NASDAQ: KTOS) — The CCA Contender

Kratos at $12.6bn market cap sits at the intersection of tactical ISR, loitering munitions, and collaborative combat aircraft — a differentiated positioning. Its Valkyrie drone (XQ-58A) has been repeatedly used as a testbed for Air Force CCA concepts and, though it was not selected for CCA Increment 1, it is expected to compete strongly for Increment 2. The jet-powered, attritable CCA market — priced at one-quarter to one-third the cost of an F-35, or roughly $20–30m per unit — represents a $3bn+ per year R&D market at the US Air Force level alone. Kratos trades at 7.1x FY26E EV/Sales, roughly in line with the group, and carries a more established profitability profile than the smaller names.

DroneShield (ASX: DRO) — The C-UAS Specialist

Australia-listed DroneShield is the most focused counter-drone (C-UAS) pure-play in any listed market. Its DroneSentry-X and DroneGun products are deployed by multiple allied militaries. The Iran campaign has been a direct demand catalyst — every air defence conversation now includes a discussion of cost-effective C-UAS interception, and DroneShield’s portfolio sits squarely in that conversation. At A$3.6bn market cap and 10.9x FY26E EV/Sales, it is the most expensive name in the peer group on a forward basis, reflecting the C-UAS demand surge being priced in aggressively.

Unusual Machines (NYSE: UMAC) — The FPV Domestic Play

At $530m market cap, Unusual Machines is primarily a consumer and government FPV supplier. It benefits from NDAA tailwinds, having been selected for various government FPV frameworks, and its partnership with the UMAC motors used in Red Cat’s FANG F7 drone illustrates how interconnected this small ecosystem is. The revenue base is still small, the gross margins volatile, and the competitive dynamics with offshore producers are challenging. Not a high-conviction name at current multiples without clearer evidence of sustained Army/DoD volume.

The Private Universe: Who to Watch for IPOs

The most interesting companies in the drone sector are not yet public. Any serious framework for the space needs to account for them — both as future listed names and as competitive benchmarks.

Anduril (US): The defining company of the new defence tech wave. 7,000 employees, its Arsenal-1 factory ($900m investment, highly automated production in Ohio), selected for CCA Increment 1 alongside General Atomics (YFQ-44A). Its product suite spans ISR drones, loitering munitions, interceptors, undersea vehicles, and the Lattice battle management software core. Anduril is the benchmark for what a modern neo-prime looks like — hardware as the vehicle for recurring software revenues. An IPO, when it comes, will be the most consequential defence tech listing since L3 Technologies.

Shield AI (US): 1,000+ employees, with Hivemind — its specialised AI autonomy software — at the centre of its product architecture. Shield AI’s thesis is that the software that enables a drone to operate without GPS, without communications links, and in adversary-contested airspace is the most durable value layer in the stack. It is correct. The company has secured significant US DoD contracts and is increasingly operating internationally.

Helsing (Germany): The most important European defence AI company. ~1,000 employees, developing the CA-1 Europa CCA alongside tactical ISR platforms and AI software for allied military systems. Selected for early German Air Force AI integration programmes. A potential future IPO candidate in European markets.

Tekever (Portugal): 1,000+ employees, specialising in maritime surveillance MALE drones. Tekever’s AR5 system has been deployed in multiple European maritime patrol roles. Unusual in that it has set up production in the UK, filling a domestic capability gap.

Destinus (Netherlands): Focused on loitering munitions and drone interceptors. Strong Dutch government backing and rapidly expanding production capacity.

A Closer Look at One of the More Interesting Names

Red Cat is not the obvious choice for a deep dive. Its market cap sits at roughly $1.6bn — the upper end of small cap, well short of the institutional threshold for most dedicated defence funds. Its losses are significant. Its revenue history is short and lumpy. And at first glance, the valuation on trailing numbers looks demanding.

But look through to the forward numbers, and a different picture emerges. Red Cat holds the US Army’s programme-of-record contract for the Short Range Reconnaissance (SRR) programme — the Army’s flagship small drone fielding effort, covering platoon-level ISR and target acquisition. It won that contract in November 2024, defeating Skydio in a competitive multi-tranche evaluation process. The contract is currently in LRIP phase, with Full Rate Production expected to follow imminently.

In a listed universe where most names either lack government traction (UMAC), are expensively valued incumbents (AVAV), or carry CCA-phase risk (KTOS), Red Cat’s combination of Army endorsement, NDAA compliance, and accelerating revenue ramp makes it genuinely differentiated. This section builds the analytical foundation. A follow-on note will go deeper.

Company Architecture

Red Cat operates through three wholly owned subsidiaries that collectively address multiple segments of the tactical drone market:

The ARACHNID™ Family of Systems ties these together — a modular sensor-to-shooter (S2S) architecture integrating ISR drones, FPV precision-effects systems (FANG™), and a common ground control interface via ATAK. Total production footprint: 254,000 sq ft as of December 2025, a 520% increase over the prior year. The scale of the Blue Ops facility relative to Teal and FlightWave signals where management sees the longer-term volume opportunity — maritime is the adjacent market expansion play.

The Army SRR Franchise

The Black Widow is the commercial expression of Teal’s SRR win. Its competitive advantages, as validated through multi-round Army evaluation, include:

AI-aided target identification, tracking, and classification

Forward-looking obstacle avoidance

Stealth mode: full radio-off autonomous operation

Low acoustic signature

Modular payload architecture supporting secondary ISR or kinetic payloads

The Army’s acquisition objective is approximately 5,880 systems over a five-year period of performance. The LRIP Tranche 2 contract, signed July 2025, has been expanded and is now valued at approximately $35m. Full Rate Production was previously outlined in Army budget documents at approximately $220m — split roughly $148m for hardware and $70m for spares, repairs, and training. The sustainment tail is an underappreciated feature: programme-of-record contracts generate recurring revenue that persists long after the initial hardware delivery.

Red Cat has stated production capability of 500+ Black Widow systems per month, with the ability to scale further given current supply chain readiness. CEO Jeff Thompson’s commentary — “if they gave us an order for 5,000 a month, we could get there in two months” — suggests production is not the binding constraint.

Beyond the Army relationship, Red Cat has received its first order for 100 Black Widows through the NATO Support and Procurement Agency (NSPA) and has now received orders from two Asia-Pacific allied nations, validating international demand at an early stage.

The NDAA Moat

This warrants emphasis because it is easy to underestimate. The National Defense Authorization Act effectively prohibits US government agencies from procuring drone systems containing components from designated adversary nations. This structurally excludes DJI — the global market leader with estimated revenues of ~$11bn in 2024 — from the US and allied government market.

Red Cat’s entire product line is designed to comply with these restrictions. All FANG components are independently certified on the DIU Blue UAS Framework. The Black Widow is Blue UAS cleared. The TRICHON VTOL system carries the same certification. In the DoD’s 340,000-drone strike programme — the largest government FPV procurement in history — every single unit must be NDAA-compliant. Red Cat, with FANG F7 already on the DIU cleared list, is one of a handful of companies positioned to compete for meaningful volume across all four phases.

Financial Performance: The Revenue Ramp

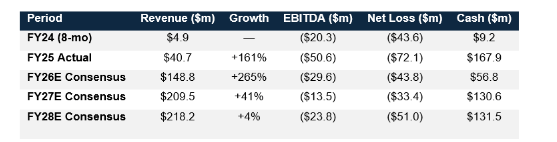

The numbers tell a story of violent inflection. Red Cat operated on a non-standard fiscal year until recently — the “FY24” period in FactSet covers only 8 months. The comparison with FY25 is therefore not clean, but the trajectory is unambiguous.

The Q4 FY25 read deserves its own emphasis: revenue of $26.2m, up 1,985% year-on-year and 172% sequentially. That is the Army LRIP deliveries landing. The implied quarterly run-rate for FY26E consensus is approximately $56m by Q4, up from $26m in Q4 FY25 — achievable if Full Rate Production is awarded and deliveries commence on schedule.

The loss profile is the most difficult part of the story to navigate. FY25 net loss widened to $72.1m on $40.7m revenue, producing a gross margin of barely 3%. The majority of this reflects the investment phase: R&D of $17.9m, S&M of $13.1m, and G&A of $36.9m were all scaled aggressively in anticipation of the revenue ramp. Consensus gross margin improvement to ~21% by FY26E ($31m on $148.8m revenue) is mathematically achievable but requires clean execution on production efficiency, supply chain management, and delivery timing.

The balance sheet entered 2025 as a concern. It exits in far better shape: cash of $167.9m at year-end after $234.3m in net equity issuance. The flip side: this is a company that has demonstrated a willingness — and necessity — to raise equity at pace. Consensus models additional financing rounds of $100m in both FY27E and FY28E. Dilution is embedded in the business model.

Valuation

The trailing 2025A EV/Sales of 15.6x looks rich. Compress to 2026E and RCAT sits closer to the drone sector median of 7.7x — despite having a more defensible revenue profile (programme-of-record) than several peers in the comp set. On 2027E, 5.4x is below Kratos and DroneShield and competitive with the broader group.

Two observations on the comp table that inform how to interpret these multiples:

First, the traditional defence names (Teledyne at 4–5x, AeroVironment at 4–5x) trade at a significant discount to the drone-specialist group. The gap reflects the “optionality premium” embedded in smaller, pure-play names — the market is pricing in a meaningful probability that companies like Red Cat and Kratos capture disproportionate share of the structural budget uplift. That premium is real, but it is not permanent. As budgets scale and the large primes (Northrop, Lockheed, L3Harris) redirect attention to unmanned systems, smaller innovators have historically seen that premium compress.

Second, Ondas’ violent de-rating from 31.7x 2025A to 4.1x 2026E illustrates how compressed multiples can become once initial hype meets execution reality. Red Cat’s de-rating from 15.6x to 7.7x is less dramatic, and it is supported by an actual delivery track record in Q4 FY25. But it is a useful reminder that multiples in this space carry real risk of compression if the revenue ramp disappoints.

Key Risks: What Would Make This Thesis Wrong

Programme concentration. FY26E consensus revenue of $148.8m is almost entirely dependent on the Army SRR Full Rate Production contract delivering on schedule. A budget sequestration, continuing resolution, or programmatic review compresses the ramp materially. DoD spending under the current political environment is more uncertain than the base case allows.

Cash burn and equity dilution. At a FCF burn rate of ~$111m in FY26E against a modelled year-end cash position of $56.8m, Red Cat requires capital market access within the year. The consensus bakes in $100m financing rounds in FY27E and FY28E. Each raise is dilutive. The share count expansion risk is not trivial.

Gross margin execution. The step from 3% gross margin in FY25 to 21% in FY26E is the most important operating assumption in the model. It requires that fixed cost absorption accelerates as volume scales and that the supply chain delivers at the implied unit economics. It has not yet been demonstrated at the required production rates.

Large prime encroachment. AeroVironment is already a partner — integrating the Black Widow into its broader mission-system architecture. That partnership can be collaborative or it can evolve into a channel where AeroVironment gradually takes share of the customer relationship. The history of defence contracting is rich with examples of small innovators whose technology was eventually internalised by a larger partner.

Technology obsolescence. Electronic warfare is advancing in parallel with drone capabilities. The jamming, spoofing, and counter-autonomy technologies being developed in response to the mass tactical drone environment could render today’s Black Widow architecture materially less effective within 18–36 months. Red Cat’s R&D spend will need to keep pace.

The FPV commodity trap. FANG competes in a segment that will ultimately be won on volume and unit cost. US government demand for NDAA-compliant FPVs provides near-term protection, but the 340,000-drone programme involves up to 12 vendors in Phase 1, narrowing to 5 by Phase 4. Red Cat needs to be in that final cohort for FANG to be a durable revenue contributor.

What Comes Next

This deep dive is explicitly positioned as a starting point. There is more work to do on Red Cat specifically — a more detailed channel check on the SRR delivery schedule, a closer look at the gross margin bridge assumptions, and a bottom-up view on which pieces of the 340,000-drone programme Red Cat is realistically positioned to capture.

The drone market more broadly will continue to evolve faster than annual research cycles can accommodate. The Iran conflict is still active. Allied procurement plans are being revised in real time.

The private company landscape — Anduril, Shield AI, Helsing — is approaching an inflection point where IPO discussions will become mainstream and the public market comparables will look very different.

Red Cat Holdings is not a finished story. It is a company at the inflection point between small-cap experiment and mid-cap institution — executing on a framework contract that could be genuinely transformative if the delivery ramp sustains. It has earned more rigorous scrutiny than it is currently getting. More to come.

If this is the kind of research you want in your inbox, consider becoming a subscriber. And if you think I’ve missed something — tell me. The best investment theses are stress-tested, not protected.

- Uncovered Alpha

Disclaimer: Military UAS market data draws on a composite of industry research estimates from multiple defence sector research firms including Teal, Roland Berger, MarketsandMarkets, and Mordor Intelligence. Drone programme and budget figures sourced from US Congressional Research Service, US Department of War budget documentation, and company filings. Company-specific data sourced from Red Cat Holdings press releases and SEC filings. This analysis is for informational purposes only and does not constitute investment advice or a solicitation to buy or sell any security. Past performance is not indicative of future results.